Regulation: How Brexit is shaping up

- Like

- Digg

- Del

- Tumblr

- VKontakte

- Buffer

- Love This

- Odnoklassniki

- Meneame

- Blogger

- Amazon

- Yahoo Mail

- Gmail

- AOL

- Newsvine

- HackerNews

- Evernote

- MySpace

- Mail.ru

- Viadeo

- Line

- Comments

- Yummly

- SMS

- Viber

- Telegram

- Subscribe

- Skype

- Facebook Messenger

- Kakao

- LiveJournal

- Yammer

- Edgar

- Fintel

- Mix

- Instapaper

- Copy Link

Posted: 13 December 2016 | Jerry Houseago | No comments yet

Jerry Houseago, Consulting Director at NSF International EMEA details what Brexit might mean and what is already happening to the food industry in the UK…

It started in January 2013 when David Cameron pledged to hold an in/out referendum on the UK’s membership of the EU as part of his general election campaign. It wasn’t the major plank of Conservative policy and later came back to haunt him on the steps of Downing Street on 24th June 2016.

A vote of 51.9% to leave was sufficient to defeat the 48.1% ‘remain’ tally as the referendum required only a simple majority. The first consequence of the vote was a change in Prime Minister, with Theresa May being elected leader of the Conservative and Unionist Party and taking office as Prime Minister on 13th July.

The longer term consequences of the referendum are that the UK must trigger the separation process by invoking Article 50 of the Treaty of Lisbon and negotiating the terms of the separation and the subsequent relationship with the EU. The Prime Minister has indicated that this will happen before March 2017. The Treaty of Lisbon then allows for a two year process to negotiate the terms, unless all remaining Member States agree to an extension of the negotiations. Some Member States have already indicated that they would not agree to this and would want the separation to proceed as rapidly as possible. A further issue is whether Parliament needs to ratify the use of Article 50 or whether the PM can exercise royal prerogative to initiate it. The government is appealing the recent High Court decision that this does require a parliamentary vote. In summary, the very earliest leave date will be January 2019.

“Brexit means Brexit”, Theresa May famously said as she entered Downing Street. It was important for her to state this early on as she had been an active ‘remain’ campaigner. However, this only means that the UK is leaving the EU, not that the terms of the separation and subsequent relationship are defined, let alone agreed by the electorate. The essence of the problem with the referendum is indeed its simplicity. The question was only leave or remain. The referendum itself did not consider or decide the terms of the continuing, separated relationship.

The enormous complexity of the challenge facing those responsible for negotiating the terms of the UK’s exit was recognised early on, but there have been few hard facts to work on. Economists, financiers, politicians and industry leaders have all had opinions as to the positive and negative consequences of Brexit, but often they have been little more than speculation. The direst predictions, such as recession, price increases and growth in unemployment have not come about – at least not yet. Although at least one Global Manufacturer has tried to impose price increases citing the weakness of the Pound as a reason, at this point it looks like we may well avoid recession. In addition, although the pound sterling has devalued, this has to an extent been mitigated by a beneficial effect on trade.

However, the government is pressing on and there is now some clarity. Theresa May has announced that there will be a ‘Great Repeal Bill’ that will revoke the European Communities Act 1972, which gave instant effect to EU law. This will be introduced in the Queen’s speech next May and take effect on Day One of Brexit. It will end the jurisdiction of the European Court of Justice in the UK and give Parliament the power to absorb parts of EU legislation into UK law and scrap elements it does not want to keep. Secondary legislation can then be used to change law as negotiations over the UK’s future relationship with its partners continue. Major amendments or new laws may be put forward in separate bills.

Brexit Secretary David Davis said, “EU law will be transposed into domestic law, wherever practical, on exit day. It will be for elected politicians here to make the changes to reflect the outcome of our negotiation and our exit.” In other words, it is likely that the majority of current EU laws will be transposed wholesale into domestic law, allowing more time to unpick and change those that we do not want to keep.

For the food industry, nothing has changed – yet. EU regulations stand until revoked, following completion of the separation process initiated by Article 50. It is unlikely that the broad direction of UK policy will change under the current government, so the deregulation agenda with more targeted inspections and more emphasis on earned recognition, will stand or even strengthen as the government seeks to shift more regulatory costs to business. Under its ‘Regulating the Future’ programme, the FSA is actively consulting with industry on the future of the Food Hygiene Rating Scheme and the form that privatised third-party certified inspections might take. The obesity strategy is an important plank of government strategy to reduce burdens on the health service and it is likely that sugar, salt and fat levels will come increasingly under fire. The pressure for product reformulation either voluntarily or mandatorily is not likely to slacken.

That said, the National Audit Office has suggested that the sheer amount of public sector resources consumed in managing Brexit will create an emergency situation, forcing government departments to decide which of their plans they have to postpone or even cancel in order to divert the necessary resources to Brexit.

If a week is a long time in politics, then two years is incredibly short for such complex negotiations. One thing that is certain is that this will be a golden time for lobbyists as interested parties see a huge opportunity to influence the future to their benefit. Regulations are bound to be at the centre of lobbying by industry, manufacturers, importers, exporters and consumer groups. Much of the criticism of the EU was about the centrally imposed regulation, such as the infamous, but fictitious, bent banana regulations.

As part of the EU, the UK was obliged to accept and implement legislation required by the EU with only limited national derogations, particularly in respect of food law. In the future, the UK will still have to comply with EU regulations when exporting there. As the EU accounts for 70% of our food exports, in many ways it makes sense to continue with the current legislation and avoid the costs of change. For example, we only recently changed the labelling requirements in December 2014, at great expense to business. 95% of our food law is in the form of EU regulations so while, for example, there may be some appeal in the domestic market of being able to avoid the nutrition box on the packaging or show the weights of goods in pounds and ounces, in reality it is probably not practical.

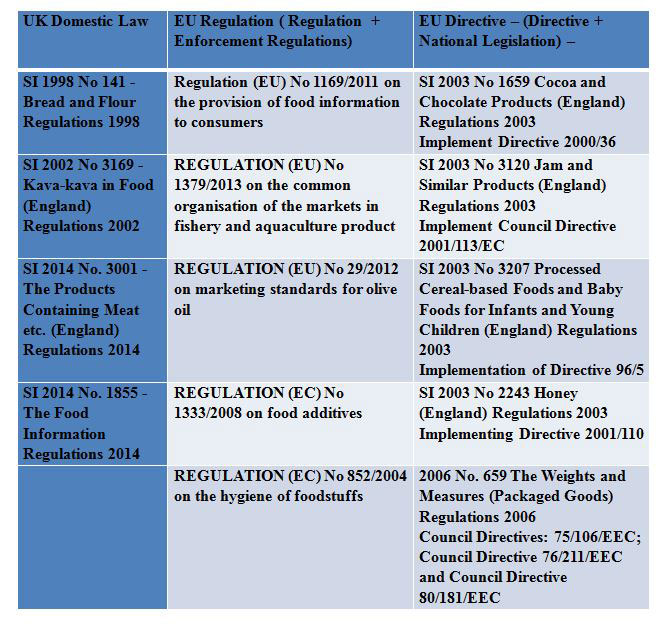

The majority of recent food law is a result of either EU directives or, more commonly, regulations. It is important to understand the differences in how directives and regulations are implemented into UK law and consequently whether or not they will be effective post-Brexit. A third method of EU law is the decision.

EU Directives: Directives set out general rules to be transferred into national law by each country as they deem appropriate. The directive is addressed to each Member State who are obliged to design and implement national legislation that meets the objective of the directive, without prescribing how that it done. Directives often have derogations, or optional requirements, so there can be national variation in implementation. This has led to the frequent criticism that only the UK has enforced EU law, creating an uneven playing field. As directives have been implemented into national law, in the UK’s case through Parliament, they will remain law post-Brexit.

EU Regulations: A regulation is similar to a national law with the difference that it is directly applicable in all EU countries. Regulations are addressed to the Member State but are directly binding on them without the need to incorporate into national law. It begs the question as to whether they will still be binding post-Brexit, and to a large degree that is where the lobbying will focus. Regulations will all require adoption into national law if they are to remain in effect, but the UK will have the opportunity to choose which they wish to retain; which to remove; and which to keep in altered form. Much of that depends on the eventual political deal as some issues are ‘red lines’ for Europe, but many others will be open to negotiation. This is essentially the reason for the Great Repeal Act and if the Government cannot achieve it legislation will need to be adopted piecemeal.

EU Decisions: A decision only deals with a particular issue and specifically mentioned persons or organisations. Decisions are best known in the food industry as the mechanism for deciding Novel Food Applications and are not well understood. Decisions only apply to the named person so if a Novel Food is authorised by a decision to Company A, then the food is only approved for Company A to market. Decisions would only remain in effect if given some UK legal authority through a UK court decision, or statutory instrument through Parliament.

Potentially, in the absence of the Great Repeal Act, we face an awkward situation whereby the UK Food Information Regulations (FIR) 2014, which provide for enforcement of the EU Food Information Regulations, remain in force whilst the EU Food Information Regulations themselves will no longer be in force, unless Parliament decides to adopt them. This is another example of the complexity of our current regulation. The EU FIR set out mandatory labelling requirements, while the UK FIR set out the sanctions and also dealt with loose food, which is not covered by EU regulations.

Therefore, in relation to Europe there are some interesting and challenging decisions to be made regarding food industry regulation. One of the major strategies of the Brexit campaign was the development of trade partnerships with other countries, with the USA being one of the most significant.

The EU has already progressed complex negotiations with the USA in the form of the Transatlantic Trade and Investment Partnership (TTIP). TTIP is specifically a trade partnership between the USA and EU, so if the UK wants a similar arrangement it will need to negotiate a separate agreement. The election of Donald Trump as the next US president could potentially reverse Obama’s warning that the “UK would go back to the queue” for a separate TTIP agreement. On the other hand Trump has shown that he is generally against reciprocal free trade agreements. Assuming the same deal can be made, what would it mean in the food sector?

The essence of TTIP is the removal of barriers to trade and increased free movement of goods without additional regulation. So product that is legal in the USA would be legal in the UK and vice versa. The theory being that it opens up markets and reduces cost. It also means UK domestic producers would face increased competition from US exporters who are currently banned from selling product by EU regulations. Currently if you want to export to the US you need to change the product labelling to meet US requirements, which is a cost but not an excessive one. However, some UK products in the UK will face competition from previously banned US imports such as GM product, dairy products reared with recombinant bovine growth hormone (rBGH), bread with potassium bromate and the Southampton seven additives. The current situation is that, after 15 negotiation rounds to date, the EU has as yet failed to agree any TTIP clauses, so it may either fail wholesale and/or the UK may get a clear field to negotiate with the US – leading some to fear an even more open and free-market solution will be detrimental to the public interest in the UK.

One thing not affected by TTIP, however, will be the impact of the Food Safety Modernisation Act (FSMA). The main provisions of FSMA – such as the Foreign Supplier Verification Programs rule; the mandatory requirement for a food defence system; and a trained preventive control qualified individual (PCQI) – would remain irrespective of the underlying ethos of TTIP to remove trade barriers.

In summary, food regulators and industry face an interesting if challenging period of negotiations. A wider question is the overall direction of international food law. Increasingly, globalised trade means that there is a drive towards simplification and harmonisation of food regulation, especially in labelling. As the UK looks to forge trading agreements outside Europe perhaps this is the bigger prize to seek. Certainly the lobbyists will be alive to the opportunities here, as the industry seeks to take the more complex and difficult – or costly – approaches to implementing rules out of the current regulations.

About the Author

Jerry Houseago is Consulting Director at NSF International EMEA. His role involves finding professional business to business solutions in food manufacturing, wholesale and retail sectors. He is a Qualified Trading Standards Officer with over 20 years experience in private sector consultancy. Jerry specialises in direct sales, sales management and provision of consultancy services related to Trading Standards, Food Safety and BRC Certification.